Clarivate announced on February 25, 2026 that it was exploring a sale of its Life Sciences & Healthcare business, and on July 6, 2026 announced a definitive agreement to sell it to Altaris LLC for $600 million. Here is what happened, what it means for the industry, and what commercial teams should consider.

What Happened

Clarivate, the analytics company behind products like Cortellis, DRG Fusion, and BioWorld, has agreed to sell its entire Life Sciences & Healthcare (LS&HC) division to Altaris LLC for $600 million — $500M cash at closing, $25M deferred against a transition services agreement, and a $75M seller note. The deal was announced on 6 July 2026 and is expected to close by the end of the year. Morgan Stanley advised on the process, which Clarivate first disclosed in February 2026.

The LS&HC business generated $389.8 million in revenue in 2025 — down 6.9% year-over-year. It is Clarivate's smallest segment, representing about 16% of total company revenue.

The stated rationale is focus: Clarivate wants to concentrate on its Academia & Government and Intellectual Property segments. Proceeds from a sale would be used to reduce debt — and Clarivate has plenty of it. The company carries roughly $4.3 billion in long-term debt with a net leverage ratio of 7.7x trailing EBITDA.

The market liked the news. Clarivate's stock jumped approximately 40% on the announcement, from $1.68 to $2.35 per share. For context, the stock traded above $33 in mid-2021. It has lost roughly 95% of its value over the past five years.

Track life sciences buying signals in real time

Clinical trials, earnings calls, leadership changes — Salesmotion monitors 1,000+ sources so your BD team never misses a trigger event.

What Is Being Sold

Clarivate's homepage — the Life Sciences & Healthcare segment is the division being put up for sale.

Clarivate's homepage — the Life Sciences & Healthcare segment is the division being put up for sale.

The LS&HC division includes some of the most established names in life sciences data:

| Product | What It Does |

|---|---|

| Cortellis | Drug pipeline intelligence, clinical trial analytics, regulatory intelligence across 80+ jurisdictions |

| DRG Fusion | Real-world data platform with commercial analytics for biopharma and medtech |

| BioWorld | Daily biotech, pharma, and medtech news and deal analysis |

| Cortellis Drug Discovery Intelligence / MetaBase | Drug discovery and curated biological-knowledge databases |

| Consulting | 300+ person team focused on market access, pricing, health economics |

These products serve the top 30 global pharma companies, plus hundreds of biotech firms, CROs, and medtech organizations. Contracts are typically six figures annually, with multi-year commitments.

“We had a variety of tools, and that was the pain — the variety. We had to go to multiple places to get streamlined data.”

Lyndsay Thomson

Head of Sales Operations, Cytel

Why This Matters Beyond Clarivate

This is not just a corporate restructuring story. It is a signal about the direction of the life sciences intelligence market.

The legacy data model is under pressure

For decades, companies like Clarivate, IQVIA, and Citeline built their businesses around curated, proprietary databases. Pharma companies paid premium prices because there was no better way to make sense of fragmented biomedical data.

That dynamic is shifting. As Christina Hein, a health AI advisor who previously led competitive intelligence at Amgen, wrote on LinkedIn:

GenAI-native platforms can now structure, query, synthesize, and reason across scientific literature, clinical trial data, patent filings, and regulatory databases at a fraction of the cost. When your competitive advantage is organized access to information, and AI learns to organize information better than you, that is not a strategy problem. That is an existential one.

This is not a fringe view. The generative AI in life sciences market was approximately $1.55 billion in 2025 and is projected to reach $45.8 billion by 2034. Pharma teams are already piloting AI-native tools alongside legacy subscriptions — and in some cases replacing them.

Ownership transitions create uncertainty

When a PE firm or strategic buyer acquires a data business, customers historically see changes in pricing, product roadmap, and support. Whoever buys Clarivate's LS&HC division will need to service $4.6 billion in parent company debt reduction expectations while maintaining a business that is already declining.

For current Clarivate LS&HC customers, this is a moment to evaluate:

- What am I actually using? Many teams subscribe to enterprise bundles but primarily use a subset of features

- What can AI-native tools handle now? Account research, signal monitoring, and meeting prep have moved dramatically in the last 18 months

- What is my cost per insight? If you are paying six figures for data that is 80% available from public sources, the math may have changed

The "interface vs. data" question

One of the most insightful questions from the LinkedIn discussion around this news came from Pablo Regueira Suarez, a life sciences market intelligence leader:

Renewal rates at the big players are still very high in big pharma accounts. AI tools will not replace companies like Clarivate and Citeline in the short/medium term as clients need to make sure that the accuracy of the tagging / proprietary ontologies are accurate.

This is a fair point — and it highlights the real trade-off. Proprietary curated data (structured regulatory filings, patient-level claims data, deep drug pipeline metadata) has genuine value that AI cannot replicate from public sources alone.

But it also raises the question Hein posed: "Which of your intelligence subscriptions are actually buying proprietary data, and which are really just buying an interface?"

For many commercial and BD teams, the answer is increasingly: the interface.

What GenAI-Native Platforms Actually Offer

The new generation of intelligence platforms does not try to replicate Clarivate's proprietary databases. Instead, they solve a different problem: making it fast and affordable for commercial teams to understand their accounts.

Here is what that looks like in practice:

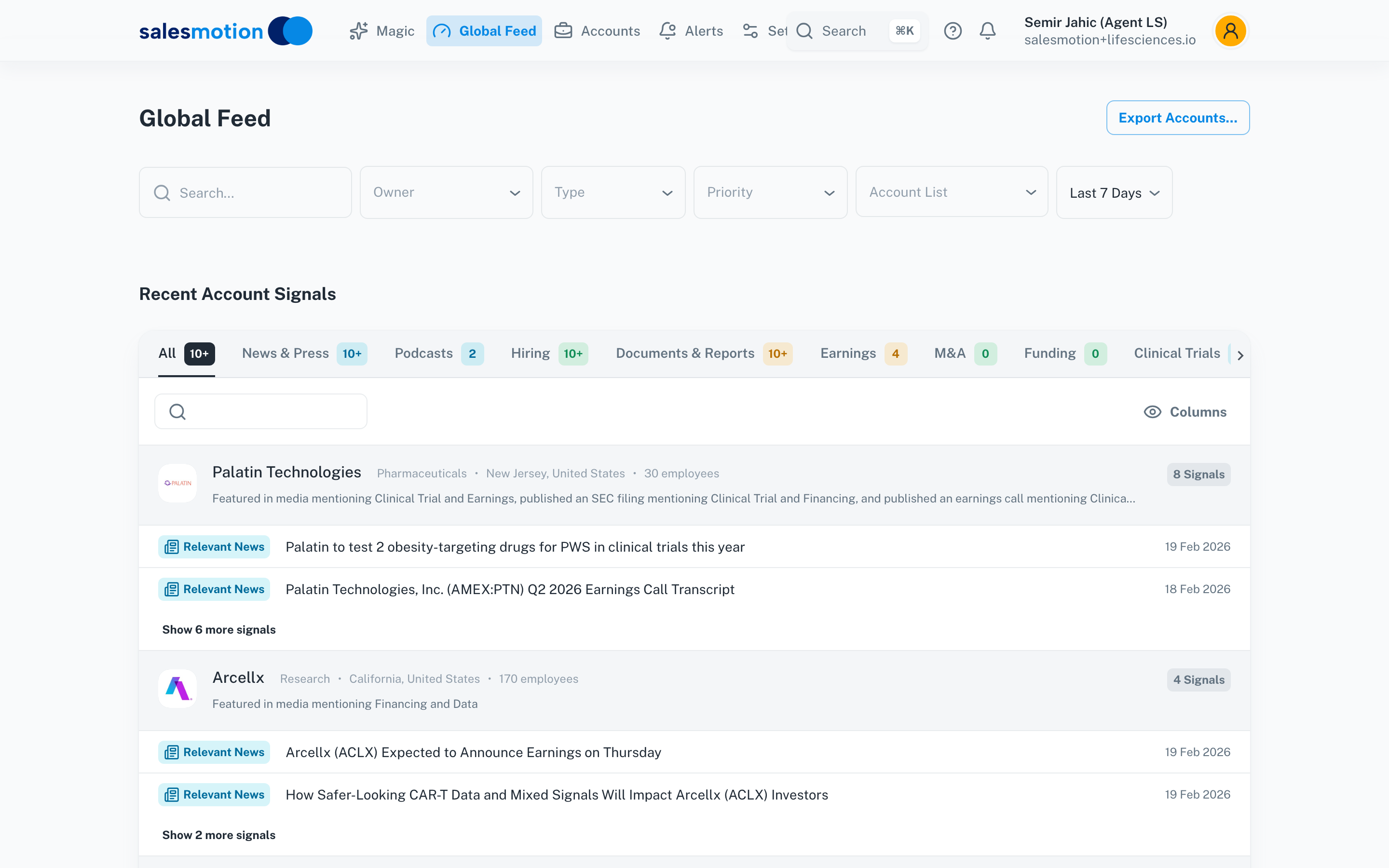

Real-time signal monitoring across life sciences accounts — clinical trials, earnings calls, leadership changes, and strategic news.

Real-time signal monitoring across life sciences accounts — clinical trials, earnings calls, leadership changes, and strategic news.

Instead of logging into multiple databases and manually piecing together account context, teams get a single feed of signals across their entire territory. Clinical trial activity from public registries, earnings call insights, leadership changes, hiring patterns, and strategic news — all synthesized by AI and tied to specific accounts.

AI-generated account briefs pull from 1,000+ public sources to give BD teams the context they need for every conversation.

AI-generated account briefs pull from 1,000+ public sources to give BD teams the context they need for every conversation.

The account brief is where the rubber meets the road. Rather than spending hours across five different tools, reps get a synthesized view of what matters — key insights, executive perspective, opportunities, challenges, and talking points — updated continuously.

Salesmotion scans and consolidates clinical trial data globally from ClinicalTrials.gov and public registries — filtered by account and contextualized for commercial teams.

Salesmotion scans and consolidates clinical trial data globally from ClinicalTrials.gov and public registries — filtered by account and contextualized for commercial teams.

“Salesmotion is helping Cytel elevate our enterprise sales performance by embedding account intelligence directly into our workflow. The platform gives our commercial team real-time visibility into key account movements.”

Jonathan Burr

Chief Commercial Officer, Cytel

The Case for Agile New Entrants

We built Salesmotion to solve exactly the problem that this Clarivate news highlights: commercial teams paying enterprise prices for data they only partially use, locked into long contracts, waiting months for implementations.

Here is the honest comparison:

What Clarivate has that we do not:

- Proprietary internally curated drug pipeline metadata (analyst annotations, structured classifications)

- Patient-level real-world claims data

- Structured regulatory filings across 80+ jurisdictions

- 300+ person consulting team

What Salesmotion delivers that Clarivate does not:

- Real-time buying signal monitoring across 1,000+ public sources

- AI-generated talking points for every account interaction

- 20-minute plug-and-play setup — no IT project, no months of onboarding

- Month-to-month pricing starting at $85/month, with unlimited users on team plans

- Cross-signal search across all accounts and all data types

- AI-drafted outreach anchored to real account research

For a detailed feature-by-feature breakdown, see our Clarivate vs Salesmotion comparison.

What Cytel Found

Cytel, a 2,000+ employee life sciences analytics company, is a good example of how this plays out. Their commercial team was toggling between 5+ tools to prepare for meetings, plan accounts, and run outreach. New hires took weeks to ramp.

After implementing Salesmotion, Cytel cut account research time by 50% and reduced account planning prep by 30%. They consolidated those five sources — ZoomInfo, Crunchbase, SEC.gov, Google News and ClinicalTrials.gov — into one. And the implementation? Their Head of Sales Operations called it the easiest vendor onboarding she had ever experienced.

“We had a variety of tools, and that was the pain — the variety. We had to go to multiple places to get streamlined data.”

Lyndsay Thomson

Head of Sales Operations, Cytel

The full story is worth reading: How Cytel Cut Sales Research Time by 50%.

Earnings call intelligence for life sciences accounts — automatically tracked, summarized, and turned into talking points.

Earnings call intelligence for life sciences accounts — automatically tracked, summarized, and turned into talking points.

What This Means for Life Sciences Sales Teams

If you are a BD or sales leader at a CRO, CDMO, biotech, or pharma commercial team, here is the practical takeaway:

1. Audit your current intelligence stack. Identify which subscriptions deliver genuinely proprietary data you cannot get elsewhere, and which are primarily serving as expensive research interfaces.

2. Separate R&D needs from commercial needs. Your regulatory affairs team may genuinely need Cortellis. Your BD team probably does not need a six-figure contract to prepare for sales meetings.

3. Evaluate modern alternatives now — not after the acquisition. Ownership transitions are the worst time to negotiate renewals. The best time to explore alternatives is before the uncertainty peaks.

4. Test the 80/20 hypothesis. Can a platform like Salesmotion give your commercial team 80–90% of the account intelligence they need at a fraction of the cost? For Cytel and a growing number of life sciences companies, the answer has been yes.

Key Takeaways

- Clarivate has agreed to sell its $390M Life Sciences & Healthcare division to Altaris LLC for $600M, expected to close by end of 2026

- The LS&HC business declined 6.9% YoY in 2025, while Clarivate carries $4.6B in debt at 7.7x leverage

- GenAI-native platforms are gaining traction in life sciences, projected to reach $45.8B by 2034

- The key question for commercial teams: which subscriptions buy proprietary data vs. an interface to public information?

- New entrants like Salesmotion offer plug-and-play account intelligence at a fraction of legacy pricing — Cytel cut research time by 50% after consolidating 5 tools

- Ownership transitions create the right moment to evaluate alternatives before pricing and roadmap uncertainty peaks

Related Pages

- Clarivate vs Salesmotion — Full Comparison

- How Cytel Cut Sales Research Time by 50% — life sciences case study

- Sales Intelligence for Pharma

- Sales Intelligence for Life Sciences

- Sales Intelligence for Clinical Research (CROs)

- Citeline Alternatives — alternatives in the pharma intelligence category

- Citeline vs Salesmotion — head-to-head comparison for biotech and pharma BD teams

- How to Sell to Pharmaceutical Companies — navigating the pharma buying committee

Sources

- Clarivate Reports Fourth Quarter and Full Year 2025 Results — Clarivate official press release

- Clarivate Explores Sale of Life Sciences & Healthcare Business — Research Information

- Why Clarivate Stock Is Skyrocketing Today — Motley Fool

- The Breakup of Clarivate — David Worlock, industry analyst

- Clarivate to Sell Healthcare Unit as Q4 Results Show Widening Organic Revenue Decline — SignalBloom

- Christina Hein on LinkedIn — original LinkedIn discussion thread

Frequently Asked Questions

What is Clarivate selling?

Clarivate has agreed to sell its entire Life Sciences & Healthcare division to Altaris LLC, which includes Cortellis (drug pipeline and regulatory intelligence), DRG Fusion (real-world data analytics), BioWorld (biotech news), Cortellis Drug Discovery Intelligence and MetaBase, and its consulting practice. The division generated $389.8M in 2025 revenue.

Who might buy Clarivate's LS&HC business?

Altaris LLC, a healthcare-focused private equity firm, is the buyer. The $600 million agreement was announced on 6 July 2026 and is expected to close by the end of the year.

Will Clarivate LS&HC products continue to work after a sale?

Yes — existing contracts will be honored regardless of ownership change. However, product roadmaps, pricing, and support models often shift after acquisitions, particularly PE acquisitions where cost optimization is a priority.

How does Salesmotion compare to Clarivate for life sciences?

Salesmotion and Clarivate serve different needs. Clarivate provides proprietary internally curated databases for R&D and regulatory teams. Salesmotion provides AI-powered account intelligence, buying signals, and meeting prep for BD and sales teams. Salesmotion actively scans and consolidates clinical trial data globally from ClinicalTrials.gov and public registries — it just does not have the proprietary internally curated metadata and analyst annotations that Cortellis adds on top. For daily BD and selling workflows, it delivers comprehensive account intelligence from 1,000+ public sources at roughly 80–90% less cost. See the full Clarivate vs Salesmotion comparison.

Is this a sign that legacy data providers are in trouble?

Not necessarily across the board, but the trend is clear. Clarivate's LS&HC revenue declined while the broader GenAI in life sciences market is growing rapidly. Companies with genuinely proprietary, hard-to-replicate data (patient-level claims, unique regulatory filings) have durable moats. Companies whose primary value is curating and organizing publicly available information face increasing competition from AI-native platforms that do it faster and cheaper.