Signal-based selling in fintech looks nothing like signal-based selling in SaaS or manufacturing. The signals that matter most to fintech sales teams are ones that traditional contact databases never track: a payments startup hiring its first compliance officer, a neobank expanding into a new geography (and suddenly needing fraud prevention), or a lending platform whose entire leadership team sits outside ZoomInfo's coverage. If your fintech sales motion still starts with pulling a contact list from a static database, you are already behind the teams that lead with signals.

TL;DR: Fintech sales teams need signals that go far beyond contact data. Expansion into new markets creates fraud and compliance buying triggers. Payment and compliance hiring patterns reveal budget allocation before any RFP appears. Many high-growth fintech prospects do not exist in traditional databases at all. A signal-based approach lets reps identify and reach these companies at the exact moment they need to buy.

Why Does Traditional Contact Data Fall Short in Fintech?

The fintech market hit $395 billion in 2025 and is projected to reach $461 billion in 2026. That growth creates thousands of potential buyers. The problem is finding them.

Traditional B2B databases like ZoomInfo were built to catalog large, established enterprises. They excel at mapping org charts for Fortune 500 banks. But fintech is not Fortune 500 banks. It is a landscape of fast-moving startups, growth-stage companies, and niche vertical players that exist in regulatory gray areas, operate across multiple geographies, and change titles and team structures monthly.

Here is what fintech sales teams consistently run into:

- Coverage gaps for niche companies. Many early-stage and mid-market fintechs simply do not appear in mainstream B2B databases. A payments company with 80 employees and $20M in ARR might have zero verified contacts in ZoomInfo. Specialized providers are filling some of these gaps, but no single platform covers the fintech landscape comprehensively.

- Title inconsistency across verticals. The person who buys compliance software at a neobank might be titled "Head of Risk," "VP of Compliance," "General Counsel," or just "COO." In a 50-person fintech, one person often owns three functions. Static title-based targeting misses these buyers entirely.

- Rapid org changes. Fintech companies restructure frequently. A Series B round often triggers a wave of new hires and title changes within weeks. By the time a database updates, the buying window has passed.

The net result: fintech sales teams that rely solely on contact data are working with an incomplete, outdated picture of their market. Signal-based selling fills the gaps that static data cannot.

What Signals Actually Drive Fintech Deals?

Not all buying signals carry equal weight in fintech. The signals that predict purchasing behavior in this vertical are specific to how fintech companies grow, get regulated, and hire. Here are the four categories that matter most.

Geographic Expansion Equals New Fraud Risk

When a fintech company announces expansion into a new market, whether that is a U.S. neobank entering the UK or a Latin American payments processor launching in Southeast Asia, it triggers an immediate chain of buying needs.

New geography means new regulatory requirements. New regulatory requirements mean new compliance infrastructure. New compliance infrastructure means new fraud detection, KYC/AML tooling, and reporting capabilities. AI-based fraud detection reduced financial losses by 40% for major platforms in 2025, which means every expanding fintech is evaluating these tools.

Geographic expansion is one of the highest-intent signals in fintech because the buying need is non-discretionary. A company cannot operate in a new market without meeting that market's regulatory requirements. The timeline is compressed, the budget is already allocated, and the decision-maker is actively searching for solutions.

Payment and Compliance Hiring Patterns

When a fintech posts job openings for payment engineers, compliance analysts, or fraud operations managers, it reveals where the company is investing before any public announcement. Research shows 85% of financial crime departments planned to hire in 2025, driven by global regulatory expansion and AI-enabled fraud detection.

Hiring signals are particularly powerful in fintech because they are leading indicators. A company does not hire a Head of Compliance for a market it is not entering. A company does not hire three payment engineers unless it is building or expanding a payments product. These signals tell you what the company will need six months from now, giving you time to build relationships before the formal evaluation begins.

Track hiring patterns for these roles specifically:

- Compliance and risk roles signal regulatory expansion or enforcement response

- Payment engineering roles signal product buildout or new payment method support

- Data engineering and ML roles signal fraud detection or underwriting model investment

- Country-specific roles (e.g., "UK Compliance Manager") signal geographic expansion

Regulatory and Enforcement Triggers

Regulatory changes create non-discretionary buying in fintech at a pace that other industries rarely match. When the EU finalized MiCA for crypto firms, when PSD3 discussions accelerated, or when U.S. state money transmitter requirements shifted, every fintech in those categories had to respond.

The data is clear on the pressure: 47% of fintechs point to unfavorable regulatory environments as a main growth barrier, and 93% say meeting compliance requirements is at least somewhat challenging. That challenge translates directly into technology purchasing.

Enforcement actions are even stronger signals. A consent order, a regulatory fine, or a public audit finding forces immediate remediation spending. These are sensitive but trackable through regulatory databases (CFPB, OCC, FDIC, state regulators). The sales team that reaches out with relevant solutions within days of an enforcement action, not weeks, wins the deal.

Funding Rounds and Burn Rate Signals

Fintech funding rebounded to $116 billion in 2025 after bottoming out at $95.6 billion in 2024. Each funding round creates a wave of technology purchases. But the signal is not just "Company X raised money." The signal is what they plan to do with it.

A Series A fintech that raises $15M "to expand its payments infrastructure" is telling you exactly what they need to buy. A Series C company that raises $80M "to enter the European market" is telling you they need compliance, fraud, and localization tools. Reading funding announcements for their stated use of proceeds turns a generic signal into a specific sales conversation.

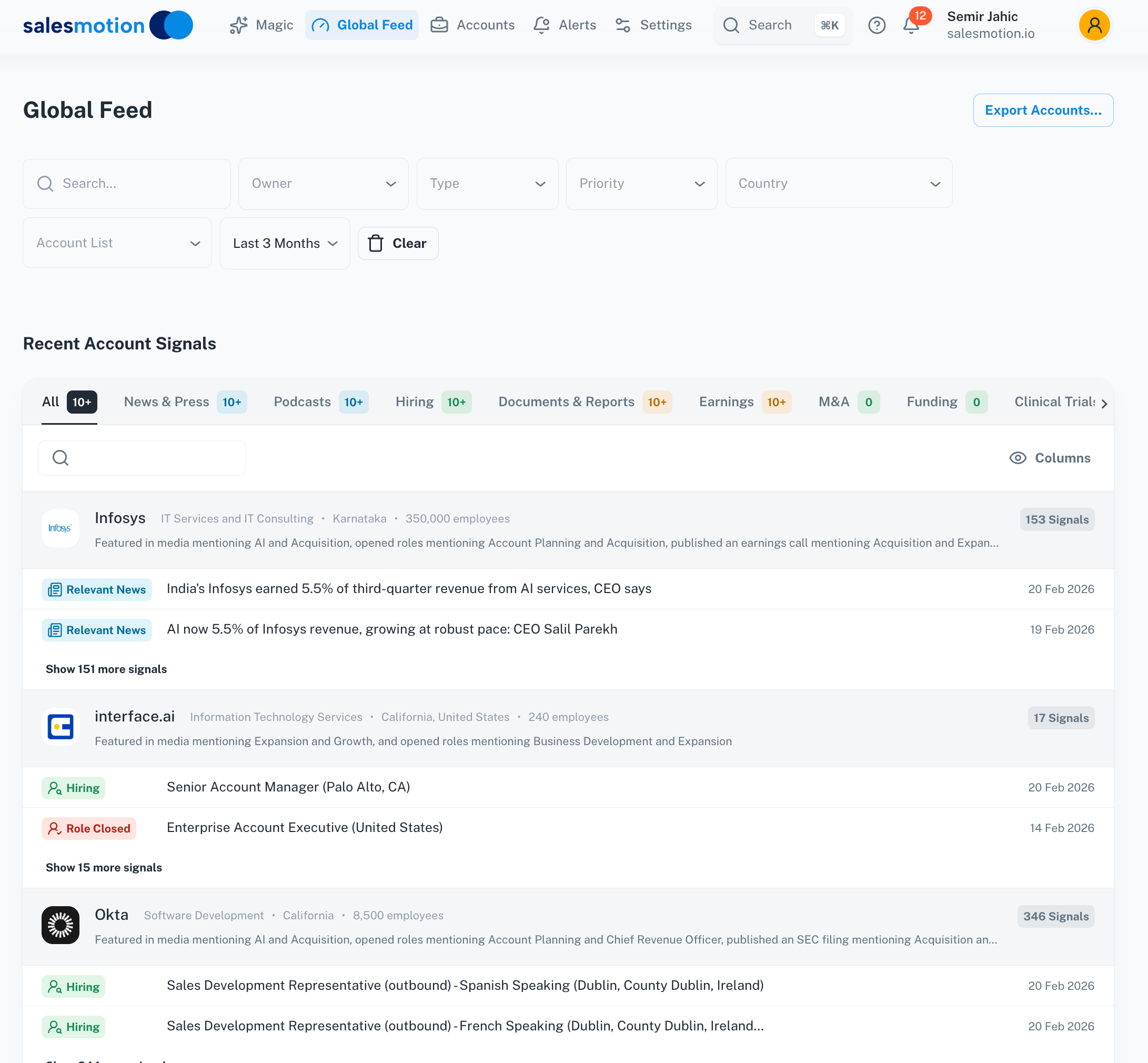

Filter your signal feed by type to surface the expansion, hiring, and regulatory triggers that drive fintech deals.

Filter your signal feed by type to surface the expansion, hiring, and regulatory triggers that drive fintech deals.

“The account and contact signals are key for reaching out at important times, and the value-add messaging it creates unique to every contact helps save time and efficiency.”

Daniel Pitman

Mid-Market Account Executive, Black Swan Data

A Signal-Based Fintech Workflow in Practice

Here is how a signal-based approach works in a real fintech sales scenario, step by step.

The trigger: A Latin American payments processor announces expansion into three new Southeast Asian markets. Your signal monitoring picks this up from a press release and cross-references it with recent job postings showing five new compliance roles in Singapore.

The research layer: You pull the company's recent regulatory filings and find they just received a payments license in one market but are still pending in the other two. Their CEO mentioned on a recent podcast that fraud prevention in cross-border payments is their "biggest operational challenge" for the year.

The connection: Instead of a generic cold email about your product, you craft outreach that references their Southeast Asian expansion specifically. You mention the fraud challenges that come with cross-border payments in those specific markets. You reference the regulatory timeline for their pending licenses and note that companies in similar situations typically need fraud detection infrastructure in place before the license is granted.

The result: The prospect responds because your message demonstrates you understand their specific situation. You are not another vendor who found their name on a list. You are someone who tracked a meaningful event, understood its implications, and connected those implications to a genuine need. Signal-qualified leads like this convert 47% better than cold outreach and produce 43% larger deals.

This is what signal-based selling actually looks like in fintech. It is not about having more contacts. It is about having better context.

Building Your Fintech Signal Stack

Implementing signal-based selling for fintech requires monitoring sources that generic sales tools ignore. Here is a practical stack:

Regulatory monitoring. Track CFPB enforcement actions, OCC bulletins, state regulator announcements, EU regulatory updates (MiCA, PSD3, DORA), and APAC financial authority publications. Set alerts for your target accounts and their competitors.

Hiring intelligence. Monitor job boards, LinkedIn, and company career pages for the role categories listed above. Pay special attention to leadership hires, as a new Chief Compliance Officer or VP of Payments almost always precedes a technology purchasing cycle.

Funding and M&A tracking. Go beyond the headline number. Read the press release for stated use of proceeds, investor commentary, and expansion plans. Cross-reference with geographic expansion signals.

News and press monitoring. Track product launches, partnership announcements, and conference appearances. A fintech that announces a partnership with a new banking sponsor is about to need infrastructure it did not need yesterday.

Account intelligence platforms. Tools like Salesmotion aggregate signals from 1,000+ sources and surface them as actionable alerts, so your team does not need to manually monitor dozens of regulatory databases, job boards, and news feeds. The platform's strength in fintech specifically is pulling together niche signals that traditional databases miss entirely.

The goal is not to monitor everything. The goal is to monitor the signals that predict purchasing behavior for your specific product. A fraud detection vendor should weight geographic expansion and compliance hiring signals heavily. A payments infrastructure company should weight funding rounds and payment engineering hires. Prioritize signal types based on your buyer persona and your average deal trigger.

See Salesmotion on a real account

Book a 15-minute demo and see how your team saves hours on account research.

Selling to Companies That Do Not Exist in Your Database

One of the defining challenges in fintech sales is that many of your best prospects are not in any traditional database. Nearly 70% of fintech leaders report persistent talent shortages, which means these companies are growing faster than databases can catalog them.

This is where signal-based selling becomes not just an optimization but a necessity. Signals surface companies that contact databases miss:

- A regulatory filing for a new payments license reveals a company you have never heard of

- A job posting for a "Head of Fraud Operations" at a company with no ZoomInfo profile tells you there is a buyer with budget

- A conference speaker list from Money20/20 or Finovate includes companies that launched six months ago

Accounts with three or more active signals convert at 2.4x the rate of single-signal accounts. In fintech, stacking signals is especially powerful because each signal type validates the others. A company expanding geographically AND hiring compliance roles AND recently funded is not a maybe. It is a high-priority account.

The vendor contacted first wins 8 out of 10 deals, according to 2025 B2B buyer research. In fintech, where sales cycles stretch 6 to 18 months and buying committees include IT, legal, compliance, and multiple executive layers, getting there first with relevant context is the entire game.

Key Takeaways

- Traditional contact databases have significant coverage gaps in fintech, missing niche companies, inconsistent titles, and rapid org changes

- Geographic expansion is one of the strongest fintech buying signals because it creates non-discretionary compliance and fraud prevention spending

- Payment and compliance hiring patterns are leading indicators that reveal budget allocation months before formal evaluations begin

- Regulatory enforcement actions create compressed buying timelines where speed of outreach determines who wins the deal

- Signal stacking (combining expansion + hiring + funding signals) produces the highest conversion rates in fintech sales

- Many of the best fintech prospects do not exist in traditional databases, making signal-based discovery a necessity rather than an optimization

Frequently Asked Questions

What makes signal-based selling different from intent data in fintech?

Intent data typically tracks anonymous web activity, such as which companies are researching topics related to your product. Signal-based selling is broader. It includes intent data but also incorporates hiring patterns, regulatory filings, funding announcements, geographic expansion, and enforcement actions. In fintech, the most valuable signals often come from regulatory databases and job postings, not website visits. Intent data tells you someone is researching a topic. Signals tell you why they need to buy and when.

How do you sell to fintech companies that are not in ZoomInfo or similar databases?

Start with signals rather than contacts. Monitor regulatory filings for new license applications, track fintech-specific job boards and career pages, follow conference speaker lists and accelerator cohorts, and watch funding announcement databases. Once you identify a target company through signals, use LinkedIn, company websites, and press coverage to map the buying committee. Many fintech sales teams find that signal-first prospecting surfaces higher-quality accounts than database-first approaches because it identifies companies at their moment of need.

Which fintech signals indicate the shortest time to purchase?

Regulatory enforcement actions and consent orders typically create the shortest buying timelines because remediation is mandatory and often time-bound. Geographic expansion with pending license applications is next, as companies need infrastructure in place before they can operate. Leadership hires in compliance or payments functions often indicate a 3 to 6 month purchasing window. Funding rounds create a broader window, typically 6 to 12 months, as companies deploy capital across multiple priorities.

How many signals should a fintech account have before outreach?

Accounts with three or more active signals convert at 2.4x the rate of single-signal accounts. For fintech, a strong signal combination might be: recent funding plus geographic expansion plus compliance hiring. However, a single high-intent signal like an enforcement action or a specific leadership hire can justify immediate outreach on its own. The key is signal quality over signal quantity. One regulatory enforcement action is worth more than five minor news mentions.