Financial services is one of the most lucrative but hardest-to-penetrate B2B verticals. Banks, insurance companies, asset managers, and fintechs spend billions on technology, but reaching their decision makers requires navigating layers of compliance, procurement bureaucracy, and organizational complexity. B2B contact data for financial services sales must account for strict regulatory environments, conservative buying processes, and the unique title structures that characterize this industry.

TL;DR: Financial services contact data requires compliance-aware sourcing, deep coverage of risk/compliance/technology roles, and real-time monitoring for leadership changes and regulatory shifts that create buying windows. Generic B2B databases cover basic contacts but miss the specialized roles that drive purchasing decisions in regulated industries.

Why Financial Services Contact Data Is Different

Three structural realities make selling into financial services fundamentally different from other B2B verticals.

Regulatory requirements shape the buying process. Every technology purchase at a bank or insurance company involves compliance review. GDPR, SOX, DORA, and industry-specific regulations like the OCC's guidance on third-party risk management add layers to every vendor evaluation. The contacts who matter most are not just the technology buyers but also the compliance officers, risk managers, and legal counsel who must approve every new vendor.

Procurement is centralized and formal. Large financial institutions run structured procurement processes with RFPs, vendor scorecards, and multi-stage evaluations. The technology leader who wants your product must get buy-in from procurement, compliance, information security, and often a steering committee. Your contact data must cover this entire chain, not just the end user or the technology leader.

Title structures are conservative and hierarchical. Financial services companies use traditional corporate hierarchies with Managing Directors, Senior Vice Presidents, and Executive Vice Presidents. The same functional role might be a "Managing Director of Digital Transformation" at one bank and a "Senior Vice President, Innovation" at another. These titles do not map cleanly to the standard title filters in B2B databases.

See Salesmotion on a real account

Book a 15-minute demo and see how your team saves hours on account research.

Key Decision Maker Roles in Financial Services

Five roles form the core of most technology buying committees at financial institutions.

Chief Technology Officer (CTO)

The CTO owns the technology strategy and architecture. At large banks, the CTO role may be split between a group CTO (strategy) and divisional CTOs (execution). Targeting the right CTO layer is essential because group-level CTOs rarely evaluate individual tools.

Chief Information Security Officer (CISO)

The CISO is increasingly a power player in financial services technology decisions. Any product that touches data, infrastructure, or customer information requires CISO approval. In many institutions, the CISO has effective veto authority over technology purchases regardless of the sponsoring department. For security-adjacent products, the CISO is the primary buyer.

Chief Compliance Officer (CCO)

The CCO ensures the organization meets regulatory obligations. They influence technology purchases related to AML/KYC, regulatory reporting, risk management, and data governance. Missing this contact means discovering compliance requirements late in the sales cycle, often after significant work has already been invested.

Head of Digital / Chief Digital Officer

This relatively new role leads digital transformation initiatives at banks and insurance companies. They own budgets for customer experience, digital channels, and process automation. Because the role is new, it is inconsistently titled across organizations, making it hard to find through standard database searches.

VP of Operations

The VP of Operations manages the day-to-day technology infrastructure that runs the business. They evaluate tools that improve operational efficiency, reduce manual processes, and support scalability. In mid-size fintechs, this role often combines technology and business operations under a single leader.

“The Business Development team gets 80 to 90 percent of what they need in 15 minutes. That is a complete shift in how our reps work.”

Andrew Giordano

VP of Global Commercial Operations, Analytic Partners

Data Quality Challenges in Financial Services

Four data quality issues are especially acute in this vertical.

Contact information is heavily guarded. Financial institutions are protective of employee contact data for security reasons. Many use internal-only directories, restrict LinkedIn profile details, and do not publish organizational charts. Direct dial numbers are particularly scarce, and mobile numbers are almost never available through standard data providers.

Organizational structures are deep and complex. A large bank may have hundreds of VPs and SVPs across dozens of business units. Knowing that someone is a "VP at JPMorgan" tells you nothing about their budget authority, business unit, or decision-making role. Your contact data needs business unit and functional area context, not just name and title.

Regulatory changes create rapid reorganization. New regulations can force financial institutions to create entirely new functions, hire specialized teams, and restructure reporting lines within months. When the EU Digital Operational Resilience Act (DORA) took effect, banks across Europe created new operational resilience teams and hired dozens of specialists. Static databases did not reflect these changes for months.

Fintech turnover is extremely high. While traditional banks have relatively stable leadership, the fintech segment experiences startup-level turnover. Executives move between fintechs frequently, and companies pivot, merge, or shut down at a rapid pace. Contact data for fintechs requires significantly more frequent verification than for established institutions.

Where to Find Financial Services Contacts

No single source provides complete coverage of financial services buying committees. The best approach layers multiple channels.

Industry-Specific Sources

Platforms like RelPro and S&P Capital IQ provide deep coverage of financial services executives. Banking and insurance trade publications like American Banker and Insurance Journal regularly report on leadership changes. Conference attendee lists from events like Money20/20, Finovate, and SIBOS offer high-quality contacts with built-in relevance.

Regulatory Filings

Public financial institutions file proxy statements, 10-Ks, and other documents that list key executives and their compensation. SEC EDGAR is a free source for this data. For a detailed guide on using regulatory filings for account research, see our DEF 14A guide.

Signal-Based Monitoring

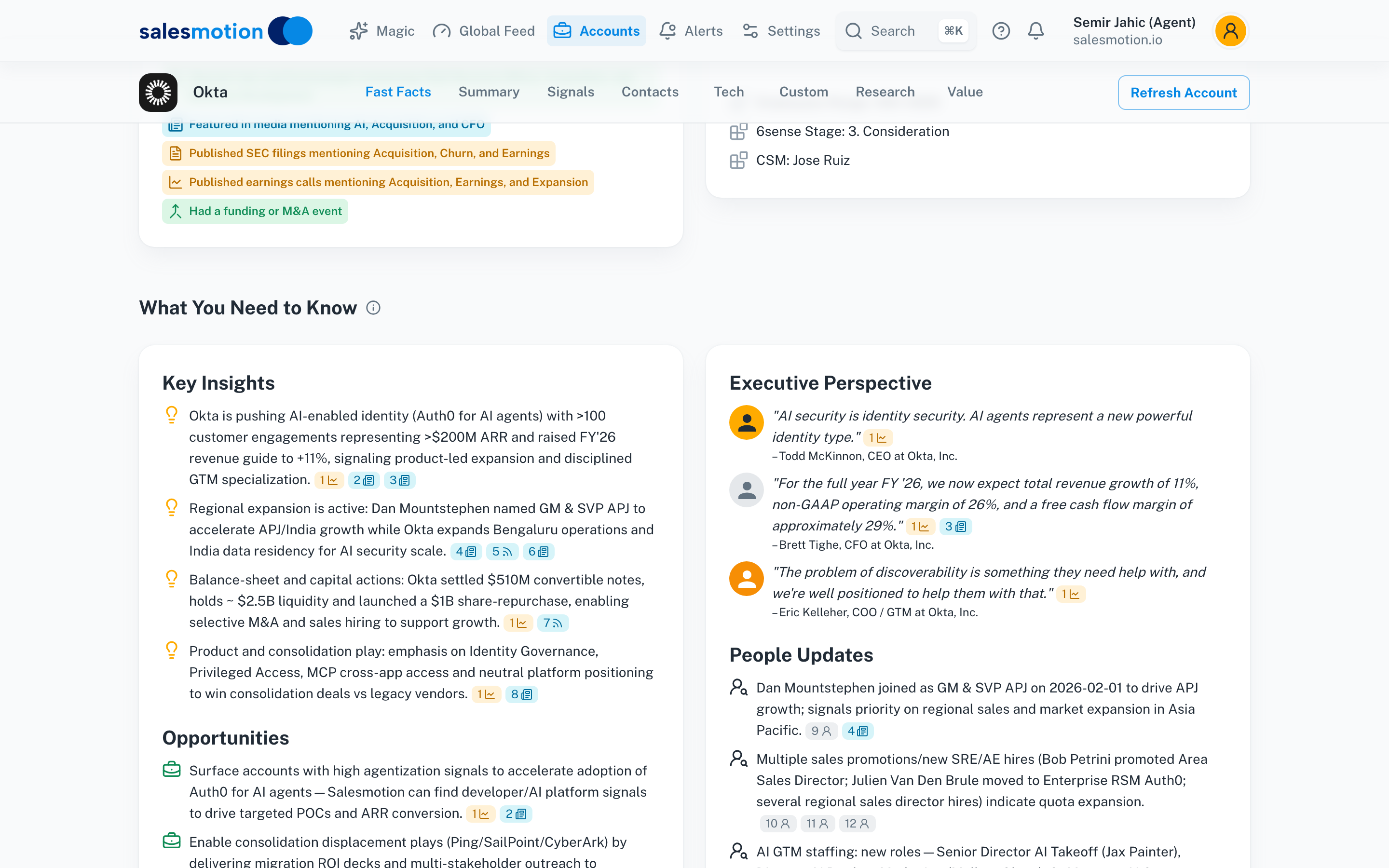

Financial services leadership changes are significant buying events. When a bank hires a new CISO, they typically evaluate and replace vendors within the first 12 months. Salesmotion monitors these transitions across financial institutions, surfacing the new hire's background, the institution's recent strategic announcements, and the contacts who report to the new leader.

Salesmotion surfaces key insights, executive perspectives, people moves, and talking points — giving reps the context behind every contact.

Salesmotion surfaces key insights, executive perspectives, people moves, and talking points — giving reps the context behind every contact.

Professional Networks and Associations

Organizations like the Bank Administration Institute (BAI), the Global Association of Risk Professionals (GARP), and ISACA maintain member directories. Board membership and committee participation lists are publicly available for many professional organizations and provide contacts with verified seniority and specialization.

“We have very limited bandwidth, but Salesmotion was up and running in days. The template made it easy to load our accounts and embedding it in Salesforce was simple. It was one of the easiest rollouts we've done.”

Andrew Giordano

VP of Global Commercial Operations, Analytic Partners

Financial Services Contact Data: Source Comparison

| Source Type | Coverage | Accuracy | Cost | Best For |

|---|---|---|---|---|

| General B2B databases | Broad, thin on FS-specific roles | Moderate (60-70%) | $15K-$60K/yr | Initial prospecting |

| Financial data platforms (S&P, RelPro) | Deep on senior executives | High (filing-verified) | $20K-$80K/yr | Executive-level targeting |

| Regulatory filings (SEC EDGAR) | Narrow, top executives only | Very high (legally required) | Free | Public company leadership |

| Signal-based platforms | Real-time, context-enriched | High (verified + timestamped) | Mid-market pricing | Leadership transitions, buying windows |

| Trade conferences (Money20/20, SIBOS) | Narrow, high-intent | High (self-reported) | Event registration | Relationship-based selling |

Building a Financial Services Prospecting Workflow

Effective financial services prospecting requires patience and precision. Here is how a signal-driven approach works.

A mid-size regional bank announces a new Chief Digital Officer hire from a large national bank. Salesmotion flags the account and surfaces context: the new CDO's background in digital lending at their previous institution, the bank's recent earnings call commentary about investing in digital transformation, and three recent job postings for digital product managers.

The rep reviews the account brief and identifies the CTO, CISO, and VP of Operations as adjacent stakeholders. The outreach to the new CDO references their digital lending background and the bank's stated digital priorities. The message to the CISO addresses security considerations proactively. Each touch is tailored to the individual's role and concerns.

This approach works because financial services buyers expect thorough preparation. A generic email to a bank CTO signals that you do not understand their world. A personalized message that references their institution's strategic priorities signals competence and respect for their time.

For a broader comparison of B2B contact data providers, see our full guide. For signal-based approaches to financial services, see our post on buying signals in sales.

Key Takeaways

- Financial services buying committees include compliance, risk, and procurement contacts that standard B2B databases rarely cover

- CISO influence is growing in financial services, with effective veto power over technology purchases that touch data or infrastructure

- Regulatory filings (SEC EDGAR, proxy statements) are free, high-accuracy sources for public company executive contacts

- Leadership transitions at financial institutions create 12-month buying windows as new executives evaluate and replace vendors

- Fintech contact data decays at startup-level rates, requiring more frequent verification than established institution contacts

- Signal-driven outreach that references institutional priorities and leadership backgrounds significantly outperforms generic campaigns

Frequently Asked Questions

How do I get past gatekeepers at banks and financial institutions?

Financial institutions use formal procurement processes that cannot be bypassed. The most effective approach is to build multi-threaded relationships across the buying committee. Start with the business sponsor (CTO, Head of Digital), get their internal advocacy, then engage compliance and procurement proactively. Sending a cold email to the CISO or CCO without an internal champion rarely succeeds.

What compliance considerations affect financial services contact data?

Financial services contact data sourcing must comply with GDPR (for EU contacts), CCPA (for California contacts), and potentially industry-specific regulations. Using data from scraping or unauthorized sources can create legal risk for your organization and damage trust with compliance-sensitive buyers. Stick to opt-in databases, public filings, and professional network data. For more on compliance-aware sales intelligence, see our glossary.

How often do financial services contacts change roles?

Traditional banks have relatively stable C-suite leadership, with average tenures of 4-6 years for senior roles. VP and SVP-level contacts change more frequently, roughly every 2-3 years. Fintechs experience much higher turnover, with average tenures closer to 18-24 months for senior leadership. Monitor these transitions because new leaders are 3-5 times more likely to evaluate new vendors within their first year.

What are the strongest buying signals in financial services?

The strongest signals are: new leadership hires (especially CTO, CISO, CDO), regulatory changes that force technology upgrades, merger and acquisition activity that requires system consolidation, and earnings call commentary about digital transformation or operational efficiency investments. These signals indicate both budget availability and organizational readiness for change.